Lessons Learned:

- Being the "best of the worst" still means you are pretty bad

- #1 IPO of 2003 on Nasdaq. Short-term success, long-term failure

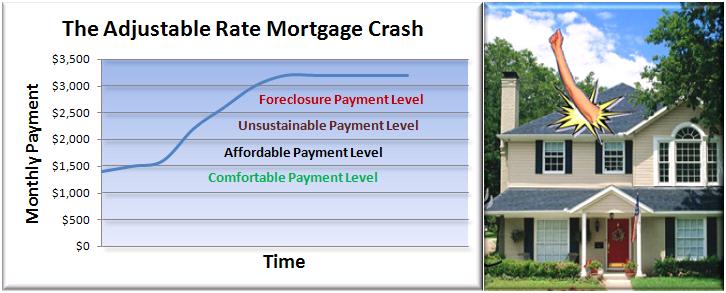

- If your business doesn't benefit the consumer in the long-run (3o years), it might not be around. Foreclosures and late payments are not beneficial to the consumer

- They had much higher rates than all of the other Sub Prime lenders. When pricing for risk - higher rates don't mean squat if you are over the consumer's threshold to pay.

- As far as I know, they did not do the Option ARMs. Types of loans that they did do: Stated Income, 100% financing ARMs

Sample Guidelines during 2005/2006:

- 580 Credit Score - Full Documentation (W-2's) - 100% financing loan

- 620 Credit Score - Stated Income - 100% combo financing loan

- 600 Credit Score - 1 day out of Bankcruptcy, 90 days late on mortgage, Full Doc - 100% financing loan

- They required more credit tradelines and rental verification than most other companies for these credit score thresholds.

Ethics:

- Heads of Corporate admitted that they had a former employee in 2004/2005 who closed multi-million dollars of loans per month actively committing fraud (creating false income documents) on a certain percentage of these. Employee was fired and began to work for another company. As far as I know, this was not reported to authorities. At least they fired him...

Source: http://www.accredhome.com/